WASHINGTON — Behind the counter at Compass Coffee, Spencer Young takes orders, makes drinks and works the kind of full-time schedule many college graduates hope will lead to independence.

Forty-hour weeks making coffees, teas and other drinks earn him $840 a week before taxes. In 2024, Young graduated from George Washington University, earning a Bachelor of Arts. His rent is $2,200 a month, and he still owes about $55,000 in student debt. After rent, food, bills and loan payments, he said, there is little left.

“After rent, living expenses and debt, I don’t really have anything left,” Young said.

Young, 23, is part of a generation described as both financially anxious and economically powerful.

According to a 2025 PwC analysis, Gen Z’s spending power is expected to grow to $12 trillion by 2030. But the same report said Gen Z is also facing inflation, rising interest rates, student loan payments and a difficult job market.

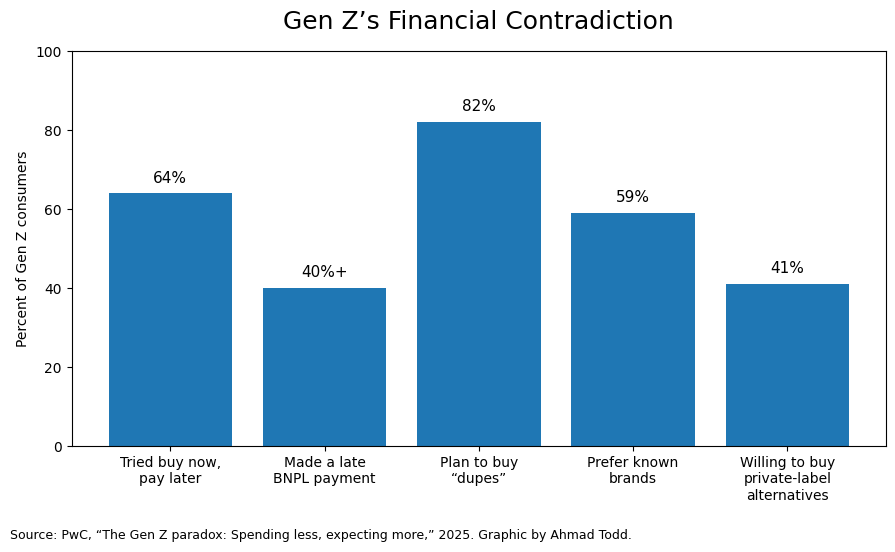

The data show a generation balancing price sensitivity with continued spending pressure. Graphic by Ahmad Todd.

Young started college in 2020, the year the COVID-19 pandemic disrupted universities across the country. He studied theater at George Washington and graduated four years later.

“I started college in 2020, so COVID was my first year,” Young said. “It was a terrible year to start.”

Now, he wants to move to New York and keeps applying for jobs there. He said he is not especially worried about the future, even though his present finances are tight. He sees this stage of life as temporary, a matter of surviving while he waits for the next one to start.

“I’m not really worried about the future,” Young said. “I think it’s just a matter of trying and trying again and surviving in the meantime.”

Similar tensions appeared in interviews with other members of Gen Z. Differences showed up in rent bills, debt payments, family support and where each person lived.

For Young, stability is enduring Washington rent while trying to enter a creative career. For Sara Jones, a sophomore at American University, money is something to be carefully managed while she focuses on school. For Jerrod McCormick, who works at Walmart in Lexington, Virginia, financial security comes from steady work, living at home and spending on the things he enjoys.

Sara Jones said she is focused on school now while preparing for internships and law school later. (Courtesy of Sara Jones)

Jones faces few costs as she studies political science with a minor in communications and works a few days a week at the front desks of AU residence halls. She makes $18 an hour and tries to keep her weekly spending under $50. Her purchases are small: coffee, occasional treats, beauty products and, occasionally, clothes.

Jones’s finances are still tied closely to school and family. Her father pays for college, she said, and she plans to go to law school, which he will also pay for.

His support gives her room to focus on academics and career preparation.

She said she applied to one internship this year because she wanted “a job for the summer in preparation for study abroad” and “some real-world experience relating to my major.”

She sees internships as useful, but not everything.

“I think they’re beneficial,” Jones said. “I don’t think they’re necessary, but I think they definitely can help with some career readiness.”

She says early career opportunities, like internships, do not always pay enough to support the students they are supposed to help. The internship she applied for was in her hometown and paid about $13 an hour, which she considered good because it was above the local minimum wage. But she said that kind of pay would not go far in Washington.

“I don’t think the internship alone pays enough at all,” Jones said. “I think like $18 an hour is definitely not enough to like pay for an apartment, especially here where it’s way more expensive than most cities.”

Jones’s financial life is cautious, but not desperate. She works, budgets and thinks about the future, but family support shields her from rent, tuition and debt. For now, her financial strategy is to spend little, build her resume and prepare for work later.

In Lexington, Virginia, McCormick’s money goes further.

Jerrod McCormick poses with a carp caught during one of his weekend fishing trips in Virginia. (Instagram)

He works at the front end of a Walmart, eight hours a day, five days a week. He makes about $15 an hour, better than the $13 he made at Kroger. He is classified as part time, which means he does not receive benefits, even though his hours resemble full-time work.

“It’s easy work,” McCormick said. “I mostly watch self-checkout, run registers, bag groceries and sometimes help with pickup orders.”

McCormick lives with his parents and does not plan to go to college or trade school. His father earns about $110,000 a year working for Dominion Energy. McCormick applied for a job there and was rejected, but he said it did not bother him.

His biggest expense is his truck, a 5.0-liter Coyote V8 Ford F-150 that gets about 17 miles per gallon. He pays around $450 a month for it.

“My truck is my pride and joy,” McCormick said.

His other major expense is fishing. He drives about 30 minutes to fish on weekends and sometimes after work. He mostly catches and releases bass, though he occasionally cooks fish wrapped in foil with lemon, butter and herbs.

“I’m always chasing the biggest bass,” McCormick said.

McCormick said he is happy and financially stable. His comfort depends on living at home and avoiding rent. Compared with Young, who earns more per hour but pays Washington rent and student loans, McCormick’s lower wage stretches further because his fixed costs are lower. Higher hourly pay does not always mean more stability.

Tapiwa Sande spoke about consumer confidence, job-market pressure and Gen Z spending habits. (LinkedIn)

Tapiwa Sande, a second-year master’s student in finance, who did research on consumer confidence and studied banking and finance as an undergraduate in Zimbabwe, said young adults are entering a job market where credentials alone may not be enough.

“For Gen Z, getting a job is no longer just about what you know,” Sande said. “It is also about who can vouch for you.”

Sande said artificial intelligence has made applications easier to polish, making personal connections more important. That can leave young workers stuck in what he described as a familiar trap.

“Gen Z is stuck in the classic catch-22,” Sande said. “You need experience to get a job, but you need a job to get experience.”

Sande said Gen Z is also being shaped by new forms of consumer credit and recurring payments. Companies such as Klarna and Affirm have made buy now, pay later programs common in online shopping. The Consumer Financial Protection Bureau said in a 2022 public inquiry that those products can appear to consumers as a standard payment option even though they are taking on debt.

“Buy now, pay later does not always feel like debt to young people,” Sande said. “It feels like a monthly payment.”

According to PwC, 64 percent of Gen Z consumers have tried buy now, pay later at least once, and more than 40 percent have made a late payment. The report described Gen Z as cautious with money but still willing to spend when a purchase feels emotionally or socially meaningful.

Sande said that can make young consumers look stable month to month while still building up obligations through rent, phone payments, subscriptions, credit cards and installment plans.

“The danger is that young people can look financially stable month to month while still becoming seriously indebted,” Sande said.

But he said Gen Z is not simply reckless. Many young adults are thinking creatively about money because they do not trust one paycheck to provide security.

“Gen Z does not only think about a nine-to-five anymore,” Sande said. “They think about investing, content creation, streaming, side hustles and online businesses.”

That does not mean every Gen Zer is living the same way. Jones is spending carefully while preparing for a professional future. McCormick is working steadily and spending on a truck and hobby he loves. Young is trying to survive expensive city life long enough to reach the next opportunity.

For Young, stability means continuing to apply. For Jones, it means staying focused on school. For McCormick, it means steady work, his truck and enough time to fish.

Source List:

Spencer Young

Barista, Compass Coffee; 2024 graduate of George Washington University

Email: S.Young2203@gmail.com

Interview date: 4/20/2026

Mode: In person

Sara Jones

Sophomore, American University

Email: sj6460a@american.edu

Interview date: 4/10/2026

Mode: In person

Jerrod McCormick

Front-end worker, Walmart (Lexington, Va.)

Phone: 540 460-8816

Interview date: 4/14/2026

Mode: Phone

Tapiwa Sande

Second-year master’s student in finance

Studied banking and finance as an undergraduate in Zimbabwe

Phone: 202 725-9728

Interview date: 05/01/2026

Mode: Phone

Vanessa

Representative, Consumer Financial Protection Bureau

Phone: 855-411-2372

Interview date: 4/30/2026

Mode: Phone

Reference List:

PwC. “The Gen Z paradox: Spending less, expecting more.” 2025.

Consumer Financial Protection Bureau. “Our public inquiry on buy now, pay later.” 2022.

McKinsey & Co. “Mind the Gap: Why Gen Z cons umers are a force to reckon with.” 2025.